Estate plans are more than your monetary net worth. Categories of your estate can include real estate, pets, possessions and all other property you own. Some people forget how priceless personal property, such as family heirlooms and keepsakes, can be to those you leave behind.

It is important to work out what will happen to these valuable items after your death by creating an estate plan.

Heirlooms have been passed down to family members for generations. These items can vary in monetary value, but the memories attached to them are copious, giving them an emotional and sentimental value that shouldn’t be discarded or auctioned after your passing.

Keepsakes are slightly different from heirlooms because they apply to specific items you owned during your life. These items can be anything from cutlery sets, furniture, or jewelry that you left behind for your family. While these valuable items only have been passed down once, they have nostalgia your family wouldn’t want to lose.

Family members can have different values associated with certain heirlooms and keepsakes. It can be crucial to talk with each family member about their feelings and expectations towards certain items in advance. This common knowledge will help your family avoid unnecessary fighting for heirlooms or keepsakes after your death.

It is a good idea to decide if you need to have your family heirlooms or keepsakes appraised. By doing this, you provide your heirs with the necessary documentation to understand the value of each object passed down to them. Plus, you might realize you want to get some of these items insured due to their worth. Handling this before you pass will make it easier for your heirs to go through the mourning process and avoid unnecessary externalities.

There is no proper way to distribute these valuable and irreplaceable items after your death. Of course, these valuables could end up lost or undervalued if they end up in the wrong hands when there is no plan in place for family heirlooms and keepsakes.

Here are some ways to distribute these precious items to your heirs.

Some people prefer to equally distribute heirlooms and keepsakes to their heirs by focusing on each items' monetary value. An estates planning attorney can offer you guidance when understanding the liquidity of each family heirloom and keepsake.

It is important to note more than two of your heirs may desire the same heirloom or keepsake. You can resolve this dilemma before you pass by creating a personal property memorandum. This document is a chance for you to explicitly state your wishes and avoid any conflict that may come after your death.

One benefit to this type of inheritance planning is that a property personal memorandum is referred to as your last will and identifies who is to receive said property. Also, you don't need to execute a new will or amend your trust if you decide to make modifications to which heirs receive these family heirlooms and keepsakes.

You may prefer to gift special items to your heirs before passing away. Doing this could be a consideration if you find enjoyment in seeing how your family reacts to receiving their heirloom or keepsake.

Of course, you don't want to forget the gift tax you may incur after giving any items to your heirs while alive. Furthermore, you may want to consider if you should factor them into what share of your estate your heirs receive after your death depending on their value.

Anderson Dorn and Rader’s attorneys have the expertise and knowledge to help you create an estate plan that considers all your assets. Family heirlooms and keepsakes are just one piece of the puzzle. Define all your wishes for what your heirs receive with an estate plan to help avoid conflict between your heirs later on.

Many Northern Nevadans know the dangers that come along with this time of year. A 2019 statistic showed that 17% of all accidents happen during winter conditions, highlighting an increased chance for individuals to experience an accident due to extreme weather changes. Ultimately, no matter how long you’ve lived in the region, less sunlight, alongside rain, snow, and black ice creates challenges for anyone driving on the road. While no one ever thinks they will fall victim to an accident, knowing what to do after a fender bender is crucial to ensuring a headache-free experience.

Following these guidelines can help you document the incident calmly and efficiently.

While many people believe there is no reason to immediately report minor accidents, following these steps avoids unnecessary complications and significant penalties down the road.

If an accident occurs making you unable to speak or communicate decisions clearly, you will need to have someone talk to medical professionals on your behalf. This should be a previously planned and trusted individual who would be deemed your medical power of attorney. This person will arrange treatment with doctors until you regain consciousness, so it's crucial you've assigned this power to someone. Your medical power of attorney will expedite medical treatment in the case of an emergency. Furthermore, your medical power of attorney should know where to obtain a copy of this documentation to help expedite treatment.

Opting for minimum coverage can be detrimental to your savings and property in the event of a serious lawsuit. You and your car must be fully covered to prevent this from happening. Plus, you should speak to your insurance broker to find out if umbrella insurance makes sense for you. Umbrella insurance is a low-cost way to gain extra liability coverage and protect yourself from damages that may exceed the limits of your car insurance. Umbrella insurance ensures you have access to a bigger pool of money in the event of a car crash lawsuit against you, protecting your savings and future prosperity.

After a car accident with significant property damages and medical injuries, it may feel necessary to protect your assets from excessive lawsuit demands. You may attempt to do this by transferring funds to friends and family, but be careful because this is against the law in some states. These transfers used to protect assets won’t be ignored by the courts. If considered fraudulent, court judges have the full right and power to reverse transfers. This means that these assets can be obtained by the party in the event of a successful lawsuit against you even after being gifted to a friend or family member.

Revocable trusts are used to protect your assets and trust from creditors and lawsuits after your death. Unfortunately, while some people believe that these trusts protect their assets during their life, this is a misconception and not their design. These trusts fail to completely protect your assets because you have complete control of all assets placed in a revocable trust. Your ability to control these trusts means a judge can order you to revoke the trust to pay creditors and lawsuit judgments.

However, with the guidance of an experienced asset protection and estate planning attorney, you can use properly designed strategies to enhance protection for your assets and property. That means taking the time to sit down with an experienced attorney well before an accident occurs offers you the best chance to maximize asset protection for your estates.

SPEAK WITH AN ESTATE PLANNING ATTORNEY

Contact us today to see how AD&R can provide you with the finest legacy and wealth planning advice Northern Nevada has to offer. We help get you the proper insurance and design estate planning to help you overcome unexpected lawsuits after an accident. Give us a call today so that we can help prepare you for the perils winter might bring.

To date, twenty-four states have enacted or introduced model legislation referred to as the Uniform Voidable Transactions Act (Formerly Uniform Fraudulent Transfer Act). The full text is available on the website of the Uniform Law Commission at https://www.uniformlaws.org/committees/community-home?CommunityKey=64ee1ccc-a3ae-4a5e-a18f-a5ba8206bf49.

When we think of estate planning, we often think about preparing our accounts and property to go to our loved ones in a tax-efficient way, protected from probate, disgruntled heirs, beneficiaries’ creditors, divorcing spouses, bankruptcy, and the poor spending habits of children or other beneficiaries. We rarely consider preparing for receiving an inheritance of our own.

Believe it or not, there are some essential things you must consider when you anticipate receiving an inheritance. Understanding these issues can be crucial to protect that inheritance from unnecessary taxes and outside threats like creditors, divorcing spouses, and bankruptcy.

The first way to properly prepare to receive an inheritance is to discover what you will be inheriting. Is it real estate, a 401(k), or an individual retirement account (IRA)? Perhaps it is publicly traded stock, an interest in a family business, or just simply cash from a savings account or life insurance policy.

Whatever it is, there are steps you can take today to plan to receive and manage it properly. For example, if you will receive a large IRA account from a parent, do you understand the new rules associated with inherited IRAs as implemented by the SECURE Act passed in late 2019? If not, you should educate yourself now on how to maximize the tax benefits available under the law regarding required distributions. Without an understanding of these often complicated rules, you could make an irreversible mistake and withdraw all of the IRA funds at one time, thereby substantially increasing your tax liability in the year of withdrawal. There are a variety of nuances to these rules that a tax adviser or attorney can help you understand and navigate properly.

Likewise, if you are receiving rental property as a part of your inheritance, you should consider the business of being a landlord and if you even have an interest in continuing to operate such a venture. If not, you may want to prepare to find a buyer for the property who can offer you a fair price as soon as possible. Or, at the very least, look into hiring a property management company to take over as soon as you inherit the property.

If your loved one has completed trust planning that includes establishing an irrevocable trust for you, such trusts frequently include important features that are generally referred to as powers of appointment. A power of appointment in a trust is a right, often given to the beneficiary of the trust, to gift trust property to someone else or, in some cases, to yourself. These powers are often limited to making gifts to only certain classes of people (such as the descendants of the trust makers), or they may be limited to making gifts only at death (a testamentary power of appointment) or during life (a lifetime power of appointment). Some trusts include both types of powers. These can be powerful planning tools that have been given to you through trust documents. Failure to recognize the existence of these powers can lead to unintended consequences, or at the very least, crucial missed asset protection and tax-planning opportunities.

If you know that you have been granted a power of appointment, you should attempt to obtain a copy of the relevant trust documents to carefully review and determine the nature of these powers. An experienced estate planning attorney can help you with this task. With this information, your professional advisers can properly advise you on the planning opportunities and tax consequences of the powers of appointment that may be available to you.

A common mistake made by married individuals who receive an inheritance is to commingle that inheritance with the property of both spouses. How can this be a mistake? An example may best illustrate the point:

Imagine Robin receives a cash inheritance from her deceased father of $300,000 and she and her spouse Morgan decide to use the inheritance to buy a vacation cabin in the mountains. When purchasing the property, the title company assumes that because they are a married couple, they want to take title to the property as joint tenants with rights of survivorship and the deed gets prepared and recorded accordingly. Further imagine that over the years, they furnish the property together, maintain it, and enjoy many family vacations there. One night, however, Morgan has a little too much to drink at a bar, gets behind the wheel, and causes a deadly accident that results not just in a DUI, but also in a wrongful death lawsuit. Because Morgan’s name is on the title to the property as a joint owner, Robin and Morgan discover that the family cabin is an asset that can be used to satisfy the lawsuit judgment against Morgan. As a result, they are forced to sell the cabin and use half of the proceeds to satisfy the judgment.

This unfortunate circumstance can be the result of Robin’s failure to keep her inheritance as separate property. By commingling her property with Morgan, she made it much easier for the judgment creditor in the lawsuit to reach what otherwise would have been considered Robin’s separate inheritance property.

Commingling inherited property can also lead to a similar result if Robin and Morgan ultimately divorce and the family court judge has to determine how to divide the marital property. Failing to keep the inherited property separate during marriage can often lead to that property being divided between spouses at divorce.

A fourth way for you to prepare to inherit property is by using an inheritor's trust. This is a special type of trust that can be established by the individual who will be leaving an inheritance to you. An inheritor's trust is designed to receive the inheritance that you would otherwise receive directly. It must be carefully designed and implemented to work properly, and an experienced estate planning attorney should most certainly be used in the effort. A properly drafted inheritor's trust includes the following key elements:

An inheritor's trust includes the following benefits:

An inheritor's trust can be a powerful tool to use when you anticipate receiving a large inheritance and would like to make sure that the inheritance is protected from certain tax consequences or threats from creditors.

If you would like to learn more about any of these concepts, give us a call. We would love to discuss these ideas in greater depth with you so we can help you build and protect your wealth more effectively.

In 1984, Congress issued a resolution, signed by President Reagan, establishing March 21st as National Single Parent Day: a day devoted to recognizing the dedication of single parents, who make self-sacrificial efforts to care for their children’s needs, and encouraging family members, friends, and communities to help provide an optimal environment for their children. As a single parent, you should feel proud of your efforts to nurture and care for your children. Here are a few additional things you can do to provide for your children’s future that you may not have considered.

If your children’s other parent is willing and able to care for them if you pass away unexpectedly, he or she will likely be given physical custody of the children and responsibility for their care. In the case of single parents, however, the other parent often may not be able or willing to take on this role. This is why it is crucial for you to name a guardian who will step into your shoes to provide day-to-day care for your children if something happens to you. If you do not name a person you trust, a court will step in to appoint someone. Because the person the court chooses to be your children’s guardian may not be the person you would have chosen, it is vitally important that you designate this person in advance. You can name a guardian in your will (and in some states, a separate document can be used specifically for this purpose): Although the court will still have to appoint the guardian, the court will typically defer to your wishes.

In making your decision, there are a few factors to keep in mind: Does your chosen guardian share your values and parenting style? Will your chosen guardian require your children to relocate? Does your chosen guardian have the energy and stamina needed to care for your children? Do they have the time to be an involved caregiver? Do you want more than one guardian to care for multiple children, or do you prefer for the children to stay together? It is important to weigh the importance of these considerations in making your decision.

If your children are minors, you can establish a custodial account to hold an inheritance under a law called the Uniform Transfer to Minors Act or the Uniform Gifts to Minors Act. If you do not appoint the custodian, the court will appoint someone to control and manage your children’s inheritance until they reach the age of majority. This is necessary because minors legally cannot own money or property on their own. A custodian will manage the funds in the account for the benefit of your children, but the downside is that when they reach the age of majority (18-21 years old depending on applicable state law), the funds will be distributed to them in a lump sum. At that point, they can spend the money as they wish, which may not be optimal for a young person who is not yet mature enough to make prudent financial decisions. In addition, any present or future creditors could try to reach your children’s inheritance to satisfy their claims.

A trust is often preferred over a custodial account because it is more flexible and can be designed to protect the funds against your children’s future creditors and their own imprudent spending. You can name someone who is adept at handling money to manage and disperse the funds for the benefit of your children if you die before they reach adulthood—or the age you have decided to the funds should be distributed to them. This can be the same person who will act as the children’s guardian, or a different person if you do not trust the guardian (e.g., an ex-spouse) to handle the money you have left to your children.

If you would like to set up a trust that can be used to manage your money and property for your (and your children’s) benefit if you become too ill to do it yourself, you can establish a revocable living trust with yourself as the trustee. This type of trust will remain in effect if you pass away, and the successor trustee you have named can continue to manage the funds and make distributions for the benefit of your children. The successor trustee can also step in to manage and distribute the funds for your benefit if you are unable to do so. An often less preferable option is to include provisions in your will for the establishment of a trust at your death. This type of trust will not help if you become disabled because it will not go into effect until your death. In addition, it will not be funded until your will has been probated, a process that may be expensive and time-consuming. Also, by creating the trust through your will, the management and distribution of funds may also be subject to ongoing oversight by the probate court.

The trust terms can specify the purposes for which the trust funds can be used, how and when the trustee should make distributions, and, if you so choose, the age at which you would like the trust funds to be fully transferred to your children—which does not have to be at the age of majority. You can choose the type of distributions you believe are best for your children: Some parents give the trustee the discretion to make distributions for specific purposes, such as the children’s health, maintenance, education, or support, or even for a down payment on a house or to provide funding for the child to start up a business. Others give the trustee complete discretion in making distributions for the benefit of the children. The timing of distributions, which can be designed to meet your particular goals, can also be spelled out in the trust.

If you have more than one child, you can specify whether the distributions should be for equal amounts or if a greater percentage of the money in the trust should be distributed for the benefit of certain children, e.g., children with special needs or younger children who did not get as much financial assistance from you while you were alive. In addition, you can address specific issues that may be of concern. For example, you can indicate whether you would like a home you own to be sold, or if you prefer for the children’s guardian to move into the home so they will not have to relocate. If your home is not sold, the terms of the trust can also indicate who will be responsible for paying the real estate taxes, utility bills, and maintenance expenses. The home is a particularly complex issue to consider, as there are often emotional ties and memories connected to it, as well as ongoing costs, and frequently, a mortgage. As experienced estate planning attorneys, we can help you think through the best course of action for your family.

If you have named someone other than a grandparent (your parent) to be your children’s guardian, it is important to specify in your estate planning documents whether you wish the grandparents to be able to visit with your children.

While you are living, it is your fundamental constitutional right to determine whether--and how often-- your children will see your parents (their grandparents). However, when you pass away, grandparents may have a right to see your children. Every state has enacted a grandparent visitation statute, and they vary regarding their permissiveness or restrictiveness. Some statutes only allow grandparents to obtain a visitation order when the children’s parents have separated, divorced, or one or both of them have died. Others are less restrictive1 and allow grandparents to obtain a visitation order even if the parents are still married and are both still living. What both types of statutes have in common is that they both require visitation not to interfere in the parent-child relationship and to be in the best interests of the child.

As a single parent, you can gain substantial peace of mind by creating an estate plan that ensures your children will be properly cared for—both physically and financially—in the unlikely event that something happens to you while they are still too young to take care of themselves. Please call the Anderson, Dorn & Rader office at (775) 823-9455 to schedule a consultation.

1 Some of these less restrictive statutes have been found to be an unconstitutional infringement on the fundamental right of parents to control the upbringing of their children.

Many of our clients are business owners, and indeed, Reno is a fantastic place to establish a business, whether it is a small operation or a large corporate location. There are a number of different reasons why the state of Nevada is very attractive to members of the business community.

Many of our clients are business owners, and indeed, Reno is a fantastic place to establish a business, whether it is a small operation or a large corporate location. There are a number of different reasons why the state of Nevada is very attractive to members of the business community.

One of them is the fact that there are not a lot of heavy taxes on businesses in our state. If you were to establish a limited liability company in Nevada, you would not have to worry about paying any franchise taxes or state level personal income taxes. Plus, you do not have to be a resident of the state to own or possess shares in a business in the Silver State and take advantage of these tax benefits.

The state also provides some very robust incentives in an effort to lure businesses. There are sales tax abatements on capital equipment purchases, and there are personal and modified business tax abatements. If you recycle, you get a real property tax abatement, and there is assistance available for intellectual property development and grants are available for training employees.

Another major benefit is the relatively low cost of living compared to places like San Francisco, New York, and Seattle. People that need jobs can afford to live in Reno and other cities in Nevada, so employers can find qualified workers to fill positions at all levels. Plus, if you are trying to recruit top talent, the fact that money goes a lot further in Nevada will definitely be a very useful bargaining chip.

Without question, Reno has an excellent environment for starting a business. If you decide to start a small business, you have to choose the correct business structure. The attorneys here at our firm have a great deal of expertise assisting clients that are establishing businesses. Asset protection is usually a very big concern. It is important to separate your personal assets from the assets and the actions of your business entity.

We mentioned limited liability companies previously, and as we have stated, there are definitely tax benefits in our state if you establish an LLC. The structure is also very good for protecting assets. If your limited liability company was to be sued, or if creditors were to seek a judgment against the LLC, it is very likely that your personal property would be protected. On the other side of the coin, if you were personally targeted, assets held by the limited liability company would be protected in most cases.

Another asset protection structure that can be quite useful for many people is the family limited partnership. As the name would imply, people that are involved have to be members of the same family. If you were to set up a family limited partnership, you would be the general partner, and family members that you add to the partnership would be limited partners. As the general partner, you would have sole decision-making authority.

To explain the value of a family limited partnership for asset protection, we will provide an example. Let’s say that you own three apartment complexes and a shopping center. You could convey each property into a separate family limited partnership. If there is any legal action taken against property that is held in any of these partnerships, that single family limited partnership would be targeted; the rest of your holdings would be out of play.

You could place your bank and brokerage accounts into another family limited partnership and leverage the financing so that you really do not have a lot of equity in any of the investment properties that could be attached.

The asset protection works in the other direction as well. If you or any other member of a family limited partnership was be personally sued, assets that are held by the partnership would be protected. These are a couple of business structures that are commonly utilized, but there are others. The ideal choice will depend upon the circumstances.

If you would like to learn more about any estate planning, financial planning, or elder law matter, attend one of our free Webinars. There are number of dates on the schedule, and you can click this link to obtain more information.

There are many different trusts that can be used to satisfy varying objectives. If you are concerned about the possibility of future creditors seeking to attach your assets, there is a particular type of trust that you should consider. The legal name of this trust structure is called a self-settled spendthrift trust. Among estate planning practitioners in Nevada, it is alternately referred to as a Nevada Asset Protection Trust.

There are many different trusts that can be used to satisfy varying objectives. If you are concerned about the possibility of future creditors seeking to attach your assets, there is a particular type of trust that you should consider. The legal name of this trust structure is called a self-settled spendthrift trust. Among estate planning practitioners in Nevada, it is alternately referred to as a Nevada Asset Protection Trust.

This type of trust can protect a number of different assets, including real estate, bank and brokerage accounts, personal belongings, business holdings, and other types of assets from future creditors. It may also be used as a prenuptial planning device to protect assets from spousal claims in the event of a future divorce. However, it should be noted that you cannot create a self-settled asset protection trust and convey assets into it to protect assets from creditors that already have a judgment against you.

Up until relatively recently, self-settled asset protection trusts were not legal in the vast majority of states. However, more and more states have laws on the books that allow for the creation of these trusts. Our office is in Reno, Nevada, and our state of Nevada is one of the states that does allow self-settled asset protection trusts. For your information, the other states that currently allow these trusts in one form or another are Alaska, Delaware, Hawaii, Mississippi, Missouri, New Hampshire, Ohio, Rhode Island, South Dakota, Tennessee, Utah, Virginia, West Virginia, and Wyoming.

We should point out the fact that you do not necessarily have to reside in the state where the self-settled spendthrift trust is going to be established. However, your will need to designate a trustee of the trust that resides in the state in which you are creating the trust. In addition, it is a good idea to relocate your assets to that state. This is relatively easy to do with some types of assets, like bank accounts and marketable securities. On the other hand, it is impossible to transfer real property to another state. For real property, it is recommended that you transfer the interest into a limited-liability company organized in the state in which you are creating the trust, and then transfer the membership interest in the limited-liability company to the trust. Then the trust will then own an interest in intangible personal property located in the state of the trust's creation.

When you decide to establish a self-settled or domestic asset protection trust, you are considered to be the grantor or settlor of the trust. You convey assets that you would like to protect from future creditors into the trust. It is important to understand the fact that this is an irrevocable trust, so the act of transferring property into the trust is permanent. You cannot change your mind later and take back personal possession of these assets.

The trust administrator is called the trustee, and generally speaking, the grantor of a self-settled asset protection trust would be prohibited from acting as the trustee. You would utilize an individual that you know or a professional fiduciary like an attorney, certified public accountant or the trust section of a bank or a trust company to handle the trust administration chores. The person or entity that is acting as the trustee must physically reside in the state where the trust is being created.

Once you convey assets into the domestic asset protection trust, you are not left completely out in the cold with regard to the utilization of assets in the trust. The trustee can distribute assets from the trust to you in accordance with the terms of the trust agreement. It would also be possible for the trust declaration to give the trustee the discretionary power to distribute assets to members of your family.

We should point out the fact that the trust will protect assets from future creditors, but sometimes there is a waiting period depending on the laws of the state in question. In Nevada, waiting period is two years, which is among the shortest of all the jurisdictions that recognize these trusts. So, by way of example, if you convey assets into a Nevada Asset Protection Trust today, and there is a judgment against you eighteen months from now, the assets may be fair game.

This is a relatively brief explanation of one of the many tools in the estate planning toolkit. Each case is different, and this is why personalized attention is very important. When you work with our firm, we will gain understanding of your needs, make recommendations, and help you put the ideal estate plan in place.

If you would like to schedule a consultation right now, we can be reached by phone at 775-823-9455. We are also holding a series of Webinars over the coming weeks, and you can learn a great deal about many different estate planning topics if you attend one of these information sessions.

They are free to attend, but we do ask that you register in advance to reserve your seat, because space is limited. You can check out the schedule and obtain registration information if you click the following link: Reno Estate Planning Webinars.

As Reno asset protection attorneys, we emphasize the fact that relatively frequent estate plan revisions may be necessary. There are different events that occur throughout society as a whole that can render your existing estate plan in need of adjustments. At the top of this list would be changes to the tax code that impact the estate tax and/or the gift tax.

As Reno asset protection attorneys, we emphasize the fact that relatively frequent estate plan revisions may be necessary. There are different events that occur throughout society as a whole that can render your existing estate plan in need of adjustments. At the top of this list would be changes to the tax code that impact the estate tax and/or the gift tax.

One of the things that commonly takes place in the lives of individuals is a change in marital status. As we all know, many first marriages end in divorce, and most people who get divorced eventually remarry. If you decide that you would like to get remarried after having been divorced, you may want to consider entering into a prenuptial agreement.

Of course, everyone who remarries feels as though they have found the right person, or they would not be getting married. However, some 60 percent of second marriages do not endure, and over 70 percent of third marriages end in divorce. As you can see from the statistics, it is more likely than not that your second or third marriage will not last. Is it prudent to go forward without a prenuptial agreement given these figures?

Given these statistics, you should make sure that your children from previous marriages are provided for regardless of what takes place in the future. You can provide for your new spouse while ensuring the future well-being of your children if you plan ahead in an intelligent and informed manner. This is often done through the creation of a trust called a qualified terminable interest property trust (QTIP).

When you establish this type of trust, your spouse would be the first beneficiary, and you name your children as the secondary beneficiaries. You fund the trust with property that you eventually want to pass along to your children, but your spouse could potentially utilize the property while he or she is still living. For example, if you convey your home into the trust, your spouse could still live in it.

If there are income producing assets in the trust, you could empower the trustee to distribute this income to your spouse throughout the rest of his or her life. Your surviving spouse would be well taken care of, but the terms of the trust would be set in stone with regard to the eventual transfer of the assets to your children. After the passing of your spouse, your secondary beneficiaries would assume ownership of assets that remain in the qualified terminable interest property trust.

As we stated in the opening, changes in tax laws could necessitate the need for an estate plan update. On another level, if you experience extraordinary financial success over the years, you may suddenly be faced with estate tax exposure. If you originally created your estate plan when your assets did not exceed the amount of the estate tax exclusion, you would definitely need to discuss death tax efficiency strategies with an estate planning attorney.

For the rest of 2018, the estate tax exclusion stands at $11.2 million, and the maximum rate of the tax is 40 percent. This means that the first $11.2 million can pass to your heirs free of taxation, and anything that exceeds this amount is subject to the death tax and its rather high 40 percent rate.

There are a number of different strategies that can be implemented to ease the burden. One possibility is the creation of a qualified personal residence trust. The way that it works is you convey your home into the trust, and when you do this, it is no longer part of your estate. However, there is a gift tax that is unified with the estate tax, so when the beneficiary assumes ownership of the home after the expiration of the term, the gift tax would be applicable.

On the surface, it may seem as though there is no benefit from a tax perspective, but there is a catch. You can continue to live in the home as usual after you convey it into the qualified personal residence trust. This interim is called the retained income period.

For the purposes of this example, let’s say that you remain in the home for 10 years. No one would purchase a home at full market value if they could not occupy it for a decade. The Internal Revenue Service take this into account when the taxable value of the gift is being calculated. At the end of the day, the taxable value of the gift will be far less than the actual value of the home.

We are holding a number of free Webinars over the coming weeks, and you can learn a lot if you attend one of these information sessions. Click this link to see the schedule and follow the simple directions to reserve your seat. We encourage you to act now, because space is limited.

Most clients understand that revocable living trusts are valuable components of an estate plan. But when asset protection is a primary goal of your estate plan, then revocable living trusts are not necessarily the way to go. The fact is, revocable trusts do not provide asset protection from legal claims or creditors. But, there are other options available that you should discuss with your Reno asset protection attorney.

Most clients understand that revocable living trusts are valuable components of an estate plan. But when asset protection is a primary goal of your estate plan, then revocable living trusts are not necessarily the way to go. The fact is, revocable trusts do not provide asset protection from legal claims or creditors. But, there are other options available that you should discuss with your Reno asset protection attorney.

When you create a revocable family trust, and in particular a living trust, you usually name yourself as the trustee so that you can retain control over your assets during your lifetime. That is the main reason revocable family trusts are so popular. The trust is revocable so you can make changes or revoke the trust at any point during your lifetime. Because you maintain the ability to use the trust property as you wish, to sell it or give it away without restriction, and to revoke the trust and transfer assets back into your individual name these assets essentially still belong to you. Therefore, those assets remain within reach of creditors. This is why you need the assistance of a Reno asset protection attorney if you wish to protect your estate from the reach of creditors.

One of the primary goals of revocable trusts is to avoid probate and the time and expense it requires. Unlike assets that are passed on through a last will and testament, assets in a trust are inherited without the need for probate. This can be a great benefit when you consider the cost of the probate process and the time it takes to complete the process. Probate can cost anywhere from approximately four to ten percent of the estate's full value and can take anywhere from 6 months to a year. The actual cost will vary depending on your family situation and the complexity of your estate.

Living trusts are a type of revocable trust that become effective during your lifetime, allowing you to retain control of your trust assets while you are alive. Upon your death, your successor trustee takes over control of the trust. The good thing about a revocable living trust is that your successor trustee can also take over if you become incapacitated. This type of provision can be extremely beneficial in case of illness or an emergency situation making it difficult for you to continue to manage your own affairs.

A trust is still the most common estate planning tool for asset protection, but it must be an irrevocable trust. “Irrevocable” means the terms of the trust cannot be changed later on. Because of this, the assets transferred to an irrevocable trust are considered to be removed from your estate, thereby putting them beyond the reach of creditors. Simply put, asset protection means analyzing your assets and arranging them in a way that provides the most protection possible. Done properly, you can protect all of your assets from the unexpected risk of loss, without fraud or tax evasion.

Although revocable trusts are not effective for accomplishing asset protection, there are other ways to protect your wealth through an appropriate asset protection plan. This plan must be created before claims and legal liabilities arise, though. If not, asset transactions may be seen as violations of the “fraudulent transfer” law, which could have serious consequences. Because most people cannot easily determine when a legal claim may arise, it is best to start your asset protection planning now. Once you have been served with a demand for payment or a lawsuit, it is likely too late to plan. Let a Reno asset protection attorney help you be prepared.

A common misconception most people have is that asset protection requires surreptitious transactions for the purpose of evading and deceiving. However, that is not true at all. Everyone has the right to structure their assets in a way that is financially beneficial. This can easily be done within the limits of the law. Actually, the only time fraud becomes an issue is when it is clear the intent was to hinder, delay or defraud creditors from collecting legal debts. With the help of an experienced Reno asset protection attorney, you can do it the right way.

One of the most challenging components of asset protection is determining who may be a potential creditor. The better you are at determining where potential claims may arise, the easier it will be to create an effective asset protection plan. The key is to be able to create a strategy for protection against particular claims that will limit your exposure to liability.

If you have questions regarding a revocable family trust, or any other estate planning issues, please contact Anderson, Dorn & Rader, Ltd. for a consultation, either online or by calling us at (775) 823-9455.

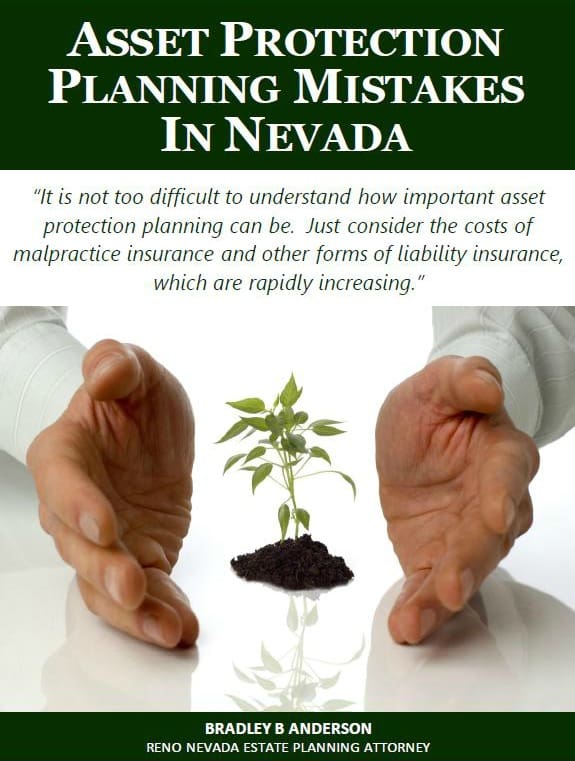

It is relatively easy to understand how important asset protection planning for Nevada residents can be. Most people want to make sure their assets are protected, including real estate, investments, business interests, and even personal property. Just consider the costs of malpractice, business (E&O), and other forms of liability insurance, which are rapidly increasing. It is certainly important to be preemptive in protecting your assets from potential creditors, whether that is through an insurance policy, homestead, or other asset protection plan. What may be even more important is understanding the most common mistakes in asset protection that Nevada residents should avoid.

It is relatively easy to understand how important asset protection planning for Nevada residents can be. Most people want to make sure their assets are protected, including real estate, investments, business interests, and even personal property. Just consider the costs of malpractice, business (E&O), and other forms of liability insurance, which are rapidly increasing. It is certainly important to be preemptive in protecting your assets from potential creditors, whether that is through an insurance policy, homestead, or other asset protection plan. What may be even more important is understanding the most common mistakes in asset protection that Nevada residents should avoid.

One common mistake that many people make is assuming that there is something wrong with creating a plan to protect your assets. Many people feel like they are "hiding assets" or irresponsibly "sheltering" their estate from the reach of creditors. That simply is not true. We are all free to structure our assets in the most advantageous way available, as long as we do so properly and in accordance with the law. The only time that the issue of fraud is raised is when the purpose of an asset protection plan is solely to hinder, delay, or defraud creditors from collecting valid debts. The key is to create your asset protection plan before the creditors' claims arise.

Plan in advance! Another mistake that some individuals make is not taking action to protect their assets until after a problem has arisen. If you've already been sued (or if you know you're about to be sued), it's likely too late to effectively create a plan. The best and most effective asset protection planning is accomplished long before any creditor claims arise. The best time to start an asset protection plan is when you are solvent and not currently facing any threats from existing creditors. The purpose of asset protection planning is to protect from potential future creditors. The sooner you start planning, the more options will be available to you.

One aspect of asset protection planning that is difficult for most people is making a proper determination of who is likely to be a potential creditor. Those who are able to make this determination are better able to make an effective asset protection plan. It is easier to plan when you know exactly what you are planning for. In other words, if you can implement a strategy to protect against certain claims you can more easily limit your exposure to that liability. Some common ways to avoid liability, especially for business owners, include:

You cannot rely on an asset protection plan someone else used. Friends may be well-intentioned, but one size definitely does not fit all when it comes to asset protection planning. Not every protection strategy will work in every case. Any estate planning attorney will tell you – an asset protection plan needs to be developed on a case by case basis. Some people can effectively create an asset protection plan by taking advantage of legal protections under homestead, ERISA, business, and other federal and local laws; still others may need a more complex asset protection trust to deal with potential creditors. Individual needs must be carefully considered when choosing your planning options, so don't use a boilerplate plan and hope that you will be protected. Most likely, you will not.

Many clients have the same misconception, that any type of trust can provide asset protection. That is not the case. First, revocable living trusts do not provide protection for individuals who created the trust simply for that purpose. It is important to remember that, in most states, when the person who has funded the trust is a potential beneficiary, then the assets may not be protected from creditors. However, a properly drafted revocable living trust may be able to add asset protection for surviving spouses and/or other beneficiaries. An irrevocable trust can only protect property that is transferred to the trust as long as there is no evidence of a fraudulent conveyance, and a statutory period of time has passed before a creditor claim arises. Foreign offshore trust accounts have come under scrutiny in United States Courts, recently. Very special care must be given when implementing an asset protection plan that includes an offshore account.

A part of asset protection planning necessarily includes consideration of possible inheritances from relatives, a factor that is often overlooked. Those inheritances must be structured, as well, in order to provide maximum flexibility, as well as, protection against creditors and divorce. An estate plan is a way for you to prepare yourself and your family for what happens after you pass away. An appropriate estate plan can also give you an opportunity to plan for unexpected incapacity. Regardless of how few assets you may have, planning for your family's future is a necessity for everyone.

If you have questions regarding mistakes in asset protection, or any other asset protection planning needs, please contact Anderson, Dorn & Rader, Ltd., either online or by calling us at (775) 823-9455.

Most clients understand that living trusts are valuable components of an estate plan. But when asset protection is a primary goal of your estate plan, revocable trusts are not necessarily the way to go. The fact is, revocable trusts do not provide asset protection from legal claims or creditors. If you have the ability to take assets out of a revocable trust as a trustee, then your creditors have the same ability to enforce a judgment against you. But, there are other options available that you should discuss with your estate planning attorney.

Most clients understand that living trusts are valuable components of an estate plan. But when asset protection is a primary goal of your estate plan, revocable trusts are not necessarily the way to go. The fact is, revocable trusts do not provide asset protection from legal claims or creditors. If you have the ability to take assets out of a revocable trust as a trustee, then your creditors have the same ability to enforce a judgment against you. But, there are other options available that you should discuss with your estate planning attorney.

When you create a revocable trust, and in particular living trust, you usually name yourself as the trustee so that you can retain control over your assets during your lifetime. That is the main reason revocable living trusts are so popular - the trust is revocable so you can make changes or revoke the trust at any point during your lifetime. This allows for flexibility to account for changes in your assets, financial status, and family. However, because you maintain the ability to use the trust property as you wish, to sell it or give it away without restriction, these assets essentially still belong to you. Therefore, those assets remain within reach of creditors.

Although revocable trusts are not effective for accomplishing asset protection, there are other ways to protect your wealth, through an appropriate asset protection plan. This plan must be created before claims and legal liabilities arise, though. If not, asset transactions may be seen as violations of the “fraudulent transfer” law, which could have serious consequences. Because most people cannot easily determine when a legal claim may arise, it is best to start your asset protection planning now. Once you have been served with a demand for payment or a lawsuit, it is likely too late to plan.

A trust is still the most common estate planning tool for asset protection, but it must be an irrevocable trust - where assets are transferred to the trust under management by an independent trustee. “Irrevocable” means the terms of the trust cannot be changed later on. Because of this, the assets transferred to an irrevocable trust are considered to be removed from your estate putting them beyond the reach of creditors. Simply put, asset protection means analyzing your assets and arranging them in a way that provides the most protection possible. Done properly, you can protect all of your assets from the unexpected risk of loss, without fraud or tax evasion. So long as a legal claim or liability doesn't arise for a statutory period of time, those assets can be kept out of the reach of creditors.

A common misconception most people have is that asset protection requires surreptitious transactions for the purpose of evading and deceiving. However, that is not true at all. Everyone has the right to structure their assets in a way that is financially beneficial. This can easily be done within the limits of the law. Actually, the only time fraud becomes an issue is when it is clear the intent was to hinder, delay, or defraud creditors from collecting legal debts.

One of the most challenging components of asset protection is determining who may be a potential creditor. The better you are at determining where potential claims may arise, the easier it will be to create an effective asset protection plan. The key is to be able to create a strategy for protection against particular claims that will limit your exposure to liability.

One of the primary goals of revocable trusts is to avoid probate and the time and expense it requires. Unlike assets that are passed on through a will, assets in a trust are inherited without the need for probate. This can be a great benefit when you consider the cost of the probate process and the time it takes to complete the process. Probate can cost between four and ten percent of the estate's full value and can take anywhere from 6 months to a year, or longer. The actual cost will vary depending on your family situation and the complexity of your estate.

Living trusts are a type of revocable trust that become effective during your lifetime, allowing you to retain control of your trust assets while you are alive. Upon your death, your successor trustee takes over control of the trust and will manage the assets as you've directed in your trust agreement. The good thing about a revocable living trust is that your successor trustee can also take over if you become incapacitated. This type of provisions can be extremely beneficial in case of illness or an emergency situation making it difficult for you to continue to manage your own affairs, and will avoid the laborious and intrusive process of petitioning for a judicial guardianship or conservatorship.

If you have questions regarding revocable trusts or any other estate planning issues, please contact Anderson, Dorn & Rader, Ltd. for a consultation, either online or by calling us at (775) 823-9455. Attend a free Webinar about revocable living trusts and their benefits!

One aspect of asset protection planning that is difficult for most people is making a proper determination of who is likely to be a potential creditor. Those who are able to make this determination, are better able to make an effective asset protection plan. It is easier to plan when you know exactly what you are planning for.

Topics covered in this report include:

Click here to read the whole article or download the PDF.

Asset protection is very important to anyone who wants to protect their estate but proper protection can be tricky. Asset protection planning is basically the process of evaluating all of your assets and arranging, or rearranging, them so you can protect them against loss. However, if not done correctly, you may cross the line into tax evasion or creditor fraud. Fraudulent transfers are a major concern in the area of estate planning.

Asset protection is very important to anyone who wants to protect their estate but proper protection can be tricky. Asset protection planning is basically the process of evaluating all of your assets and arranging, or rearranging, them so you can protect them against loss. However, if not done correctly, you may cross the line into tax evasion or creditor fraud. Fraudulent transfers are a major concern in the area of estate planning.

A fraudulent transfer, also referred to as a fraudulent conveyance, is the process of moving your assets to avoid creditors or legal liability. Whenever you convey assets for the purpose of defrauding a legitimate creditor, you are guilty of making a fraudulent transfer. The only intent required is knowing that your assets are at risk, or could be used to satisfy some legitimate legal obligation, and you move those assets out of reach.

The key is, asset protection must be done when you are not at risk, meaning you are conveying your assets when your asset protection plan is created, not when you are in some legal situation that puts your assets at risk. The problem is, even if fraud or debt avoidance is not your intent, your asset transfers may still be viewed as fraudulent, depending on the situation. It is all about timing.

For an asset protection plan to be truly effective, it must be put in place long before a creditor’s claim has been made, or any sort of liability arises. Any transactions involving your assets, which occur after the claims have arisen, are likely to be considered fraudulent. Prior planning is also important because not many people really understand or recognize when a claim of liability arises. Once you receive a demand for payment on a debt, or been served with a lawsuit, it is too late to start planning.

It is a common misconception that the only consequence of late planning is the canceling of the fraudulent transaction. Instead, both the debtor and the person who aided in the fraudulent transfer can be held liable for attorney fees incurred by the creditor involved. The debtor may also lose any chance of discharging that particular debt in bankruptcy. Many states have fraudulent transfer laws which provide very stiff penalties for fraudulent transfers.

In Nevada, a conviction for "fraudulent conveyance" is considered a gross misdemeanor, the punishment for which is up to 364 days in jail and/or up to $2,000 in fines, as well as restitution. “Receiving” a fraudulent conveyance is a misdemeanor in Nevada, resulting in up to six months in jail and/or up to $1,000 in fines, and restitution.

If a creditor can prove that you have moved your assets to avoid liability, your assets may be seized, even after they have been transferred. All a creditor has to show is that you transferred your property, you received less than fair market value for that property, and the transfer left you unable to satisfy that creditor. All three of these things must be shown. An asset protection plan goes a long way toward preventing creditors from seizing your assets, and even more important keeping you out of jail.

If you have questions regarding fraudulent transfers, or any other asset protection planning needs, please contact Anderson, Dorn & Rader, Ltd., either online or by calling us at (775) 823-9455.

Asset protection is defined as the process of examining your assets and rearranging them in a way that protects them from loss. Learn more about Nevada Assets From Lawsuits in this presentation.

Asset protection is simply the process of examining your assets and rearranging them in a way that protects them from loss. Depending on the extent and nature of your assets, your asset protection plan may be complicated. Regardless, as long as your asset protection plan is created and executed correctly, you will be prepared for the unpredictable situations that occur, which may put your estate at risk.

Asset protection is simply the process of examining your assets and rearranging them in a way that protects them from loss. Depending on the extent and nature of your assets, your asset protection plan may be complicated. Regardless, as long as your asset protection plan is created and executed correctly, you will be prepared for the unpredictable situations that occur, which may put your estate at risk.

Topics covered in this report include:

Click here to read the whole article or download the PDF.

It is important for debtors to have strategies for protecting their valuable assets from potential creditors, just as it is important for creditors to have techniques for collecting debts. Furthermore, just as creditors are required to follow the laws and regulations that govern their debt collection practices, debtors must be careful that their asset protection strategies do not cross the line into fraudulent transfers.

It is important for debtors to have strategies for protecting their valuable assets from potential creditors, just as it is important for creditors to have techniques for collecting debts. Furthermore, just as creditors are required to follow the laws and regulations that govern their debt collection practices, debtors must be careful that their asset protection strategies do not cross the line into fraudulent transfers.

The major concern in deciding when to start asset protection planning is being sure to avoid the appearance of a “fraudulent transfer.” With the help of an experienced and knowledgeable asset protection planning attorney, you can avoid the pitfalls that can get you in trouble, while you start asset protection planning for you and your family.

Start planning prior to creditor’s claims

There are many techniques for accomplishing asset protection, but they are only effective before a creditor’s claim or some other financial liability arises. The transfer of assets after a claim has arisen may be considered fraudulent. The most common example of an illegal transaction is when a debtor tries to "sell" everything to a relative for very little, solely to keep the property out of the reach of creditors.

Late planning may have serious consequences

Many clients believe that the worst that can happen is a court will undo or reverse the fraudulent transfer, leaving the client no worse off than before. In reality, both the debtor and the one who received the property, can be held liable for any attorney’s fees incurred by the creditor in collecting the debt.

What is the best way to protect assets?

Asset protection first requires looking at the nature and value of your assets and then rearranging them in a way that will maximize their protection from loss. The purpose of asset protection is not to evade taxes or defraud creditors. Instead, it simply allows you to prepare for financial situations that could possibly occur, in order to help preserve your estate for the benefit of your family.

Possibly the most common estate planning tool for accomplishing this goal is a trust. When assets are transferred to a trust, they are effectively removed from your estate. As a result, those assets are not subject to estate taxes upon your death. There are different types of trusts, with their own benefits, which can be tailored to meet the different needs and goals of each client. Discuss all of your options with your estate planning attorney to determine what will be best for you and your family. Generally speaking, trusts do not protect personal assets. But, under some circumstances an irrevocable trust may provide protection of certain assets. If you also have business assets, those need to be protected by a business entity, such as a partnership or limited liability company.

If you have questions regarding trusts, or any other asset protection planning needs, please contact Anderson, Dorn & Rader, Ltd., either online or by calling us at (775) 823-9455.

To learn more, please download our free Protect Your Nevada Assets From Lawsuits here.

Trusts are a vital wealth planning tool, not only for asset protection, but also for safeguarding the family’s wealth, regulating access to property and assets by younger family members, and providing long-term oversight and investment management for families. The trustee is responsible, either directly or indirectly, for investing those assets and making sound decisions in making distributions to beneficiaries.

Regardless of the size of your estate, it is important to consider protecting your assets and creating a plan to ensure that your family wealth will be passed on as you wish. The goal of asset protection is to shelter the wealth you have created from unnecessary risks. A family wealth trust can be the most effective and flexible option for protecting family wealth. When your estate planning attorney properly customizes a trust for your family, the benefits will far exceed simply leaving assets to family members in your will. Remember, a Family Wealth Trust is not just for the wealthy.

What Is a Trust?

A trust is just an agreement between a trustor, trustee and beneficiary regarding how and when assets will be transferred. The “trustor” is the person who owns the assets in and creates the trust. The “trustee” is the person to whom the legal title of the assets passes. The “beneficiary” is the person who eventually receives the assets after specific conditions have been met. Trustees can be friends, relatives or professionals, such as attorneys or accountants. In some cases, an entity such as a bank or a trust company can serve as trustee.

How do Family Wealth Trusts actually provide protection?

Usually, a family wealth trust becomes irrevocable when the trustor dies. This simply means its terms cannot be changed once it has been created. Furthermore, the assets are no longer part of the trustor’s estate once the trust becomes irrevocable. So, when the trustor passes away, these assets are not considered part of the personal estate and will not be subject to the beneficiary's creditors. This is only one advantage of this type of trust.

A Generation-Skipping Trust

Another option to consider is the Generation-Skipping Trust, which will allow you to retain your tax exemption on gifts to your grandchildren and avoid the tax on any amounts exceeding that exemption. In 2014, the Generation-Skipping tax exemption is $5.34 million, which is the same as the federal estate tax exclusion. This is also a beneficial estate planning tool, if you want to leave assets to your grandchildren. For instance, you can put $100,000 in a generation-skipping trust and allow it to accumulate earnings for any number of years. Still, your lifetime exemption would only be reduced by the original $100,000. If you have any questions about these or any other asset protection tools, please contact our office.