Trusts are a vital wealth planning tool, not only for asset protection, but also for safeguarding the family’s wealth, regulating access to property and assets by younger family members, and providing long-term oversight and investment management for families. The trustee is responsible, either directly or indirectly, for investing those assets and making sound decisions in making distributions to beneficiaries.

Regardless of the size of your estate, it is important to consider protecting your assets and creating a plan to ensure that your family wealth will be passed on as you wish. The goal of asset protection is to shelter the wealth you have created from unnecessary risks. A family wealth trust can be the most effective and flexible option for protecting family wealth. When your estate planning attorney properly customizes a trust for your family, the benefits will far exceed simply leaving assets to family members in your will. Remember, a Family Wealth Trust is not just for the wealthy.

What Is a Trust?

A trust is just an agreement between a trustor, trustee and beneficiary regarding how and when assets will be transferred. The “trustor” is the person who owns the assets in and creates the trust. The “trustee” is the person to whom the legal title of the assets passes. The “beneficiary” is the person who eventually receives the assets after specific conditions have been met. Trustees can be friends, relatives or professionals, such as attorneys or accountants. In some cases, an entity such as a bank or a trust company can serve as trustee.

How do Family Wealth Trusts actually provide protection?

Usually, a family wealth trust becomes irrevocable when the trustor dies. This simply means its terms cannot be changed once it has been created. Furthermore, the assets are no longer part of the trustor’s estate once the trust becomes irrevocable. So, when the trustor passes away, these assets are not considered part of the personal estate and will not be subject to the beneficiary's creditors. This is only one advantage of this type of trust.

A Generation-Skipping Trust

Another option to consider is the Generation-Skipping Trust, which will allow you to retain your tax exemption on gifts to your grandchildren and avoid the tax on any amounts exceeding that exemption. In 2014, the Generation-Skipping tax exemption is $5.34 million, which is the same as the federal estate tax exclusion. This is also a beneficial estate planning tool, if you want to leave assets to your grandchildren. For instance, you can put $100,000 in a generation-skipping trust and allow it to accumulate earnings for any number of years. Still, your lifetime exemption would only be reduced by the original $100,000. If you have any questions about these or any other asset protection tools, please contact our office.

In the case In re Estate of Karter Wu (Supreme Court of Queensland, Australia), Mr. Wu created and stored his Last Will and Testament on an iPhone, along with a series of other documents, most of them final farewells.

Wu’s iPhone Will named an executor and successor, set forth how he wished to dispose of his assets at death, dealt with his entire estate, and authorized the executor to deal with his financial affairs. The Will began with the words “This is the Last Will and Testament of Karter Wu.” At the end of the document, Wu typed his name where the testator would normally sign his name, followed by the date and his address. The Australian court admitted the Will to probate.

The law for the execution of a valid Will in Queensland, Australia, is set forth in the Succession Act of 1981. The Act provides the requirements for execution, however, it provides that, if the court is satisfied that a person intended a document to form his Will, then the document shall be considered a Will as long as it purports to state his testamentary intentions. Australian law defines a “document” to include any disc, tape, article, or any materials from which writings are able to be produced or reproduced. Citing a New South Wales, Australia, case that held a Word document stored on a laptop computer to be a document, the court held the electronic record on the iPhone was a document for purposes of the statute. Since the record contained on the iPhone named an executor, authorized the executor to deal with his financial affairs, and provided for the distribution of Wu’s entire estate at a time he was contemplating his imminent death, the court held that it met the requirements of the Succession Act 1981.

California Probate Code § 6110 provides that a Will shall be in writing and signed by the testator, or signed in the testator’s name by some other person in the testator’s presence and at the testator’s direction, or by a conservator pursuant to court order. The Will must have the signatures of two witnesses. If the Will does not meet these requirements, it shall be treated as if it did meet the requirements if the proponent of the Will establishes by clear and convincing evidence that, at the time the testator executed the Will, he or she intended the document to be his or her Will.

Similarly, New Jersey law provides at N.J.S. 3B:3-2 that a document or writing is treated as complying with the normal rules for executing a Will if the proponent of the writing establishes by clear and convincing evidence that the decedent intended the document to constitute the decedent’s Will.

The California and New Jersey statutes are based on § 2-503 of the Uniform Probate Code. The impetus for the enactment of this section of the Uniform Probate Code may have been a case where an attorney attempted to probate the unsigned draft of a Will of a decedent who was killed in the World Trade Center attack on September 11, 2001.

California Probate Code § 6130 further provides: “a writing in existence when a Will is executed may be incorporated by reference if the language of the Will manifests this intent and describes the writing sufficiently to permit its identification. California Probate Code § 6131 states: “a Will may dispose of property by reference to acts and events that have significance apart from their effect upon the dispositions made by the Will, whether the acts or events occur before or after the execution of the Will or before or after the testator’s death. . . .”

Recently, a Will was admitted to probate in California where the Will referred to the disposition of assets in accordance with recordings that the decedent had left, both prior to the execution of the Will and would leave after the execution of the Will, on his answering machine at his residence. The judge found that the recordings constituted a writing within the meaning of the California Probate Code and were to be incorporated by reference and were to be considered to be acts of independent significance. Therefore, the recordings were given effect with regard to the disposition of property as governed by the Will.

While the existence of these statutes in many states have broadened what may be admitted as a Will for probate, it is not a good idea to rely on these statutes to assure that one’s Will will be accepted by the local probate court. Having a Will drafted by an attorney experienced in estate planning and drafting is always the best course of action to assure there will be no problems with the disposition of one’s estate at death.

Furthermore, there are many reasons why one may not wish to subject his or her estate to probate upon death, including potential additional costs, delays in administration, and the publicity of both the extent of the decedent’s wealth and the identification of the beneficiaries of the estate. There are many ways to avoid a probate administration at death, including the execution and funding of a revocable or irrevocable trust during the individual’s lifetime.

For more information about the ways to avoid probate, contact our law office. Our office focuses on estate planning, probate administration, and methods to avoid probate for those who have a desire to do so. We work with clients of all wealth levels and ages. As a member of the American Academy of Estate Planning Attorneys, our firm is kept up-to-date with information regarding estate planning and estate and trust administration strategies. You can get more information about scheduling a complimentary estate planning appointment and our planning and administration services by calling Gerald M. Dorn, Esq. at (775) 823-9455

Dying “intestate” simply means you did not have a will. Each state has its own “intestate succession” laws. Nevada is no exception. How your property is distributed upon your death, depends primarily on which relatives survive you, or are still living at that time.

The Laws of Intestate Succession in Nevada.

Generally, only assets that you own alone in your name only will pass through intestate succession. Examples of property that does not pass through intestate succession, assuming the beneficiaries or joint owners are living at your death include:

Instead, these assets will pass to the surviving co-owner or beneficiary you named, whether or not you have a will.

Which relatives are in line to inherit in Nevada?

If you have children when you die, but no spouse, parents or siblings, then your children will inherit your estate. Next in line would be your spouse, parents and your siblings, in that order.

Because Nevada is a Community Property state, your spouse will inherit your share of the community property upon your death. “Community property” is property acquired while you were married, except gifts and inheritances given to only one spouse, even if acquired during marriage.

So, if you have a spouse and children who survive you, your spouse inherits all of your community property and 1/2 or 1/3 of your separate property. If only your spouse and parents survive you, they split your separate property equally, but your spouse inherits all of the community property. The same is true for siblings and a spouse, if your parents are not living at the time of your death.

Who are legally considered to be “children?”

Children who have been legally adopted receive a share along with any biological children. However, foster children or stepchildren that were not legally adopted do not automatically receive a share. Children you placed for adoption and who were legally adopted by another family are no longer entitled to a share of your estate.

Special Circumstances in Nevada

There are a few other special circumstances that warrant mentioning. Children you conceived, but were not born before your death (posthumous children) can still receive a share. Children born outside of marriage can only receive a share of your estate if it can be proven that you acknowledge them as your children and contributed to their support.

So-called “half” siblings inherit as any other sibling would. Relatives entitled to an intestate share of your property will inherit whether or not they are citizens or legally in the United States. Finally, Nevada’s “killer” rule says, that anyone who feloniously and intentionally kills you, will not receive a share of your estate. If you have any questions regarding inheritance and intestate succession, or need assistance in will drafting in Nevada, please give us call.

A very common question asked by estate planning clients is “what happens to my property if I am single when I die? The answer to this question generally depends on three things: (1) whether you have a will, (2) the laws of the state you live in and (3) which of your relatives are still alive when you pass away. This would be true even if you are married when you die. Each state has its own set of “intestate succession” laws which determine where you property will go if you die without a will. If you have a will, on the other hand, the terms of your will determine who will inherit your property.

A very common question asked by estate planning clients is “what happens to my property if I am single when I die? The answer to this question generally depends on three things: (1) whether you have a will, (2) the laws of the state you live in and (3) which of your relatives are still alive when you pass away. This would be true even if you are married when you die. Each state has its own set of “intestate succession” laws which determine where you property will go if you die without a will. If you have a will, on the other hand, the terms of your will determine who will inherit your property.

A will is an estate planning document that allows you to specify the individuals, institutions or other organizations (including charities) you want your assets distributed to when you pass away. Whether you are married or single when you die, the terms of your will always determine where your property will go. If you die without a will, or “intestate,” the laws of your state will determine how your assets are distributed.

In Nevada, if you have children but no spouse, your children will inherit everything. If your parents are living, but you have no children when you die, they will inherit everything. Likewise, if your parents are deceased and you have no children, but your siblings survive you, they will inherit everything. If any of your siblings are deceased, the share they would have received will go to their descendants.

If you do not have a will, and you have children, In Nevada they will receive what is called an “intestate share” of your estate. The size of the share will depend on how many children you have, because they will share equally. They must legally be your children; it will not go to step children. If you legally adopt a child, he or she will receive an intestate share along with any biological children. However, foster or stepchildren who have not been legally adopted do not receive a share.

If you have a child who was legally adopted by another family, that child will no longer be entitled to a share of your estate. Men who have children born outside of marriage can only receive a share if paternity has been acknowledged or proved in court. A child that was conceived by you, but not actually born before your death, will still receive a share of your estate in Nevada.

There are a few miscellaneous rules or definitions that may apply to your particular situation. For example, “half” relatives inherit as if they were “whole.” So, your brother with whom you share a mother, but not a father, will have the same right to your property as he would if you had both parents in common. Citizenship does not affect inheritance, either. Nevada also recognizes what is known as the “killer” rule, which provides that if someone commits a felony and it results in your death, that person cannot inherit any part of your estate.

If you have any questions regarding inheritance and intestate succession laws in Reno Nevada, or need assistance in will drafting in Nevada, please give us call.

You have to be concerned about taxation when you are planning your estate. Taxes on asset transfers at death are going to be a factor for many high net worth families. Nevada, however, has no inheritance or estate tax, so we only have to be concerned about the federal estate tax.

You have to be concerned about taxation when you are planning your estate. Taxes on asset transfers at death are going to be a factor for many high net worth families. Nevada, however, has no inheritance or estate tax, so we only have to be concerned about the federal estate tax.

There is an estate tax credit or exclusion. In 2014 the amount of this exclusion in this country, including Reno Nevada, is $5.34 million. Lifetime asset transfers exceeding this amount are potentially subject to a transfer tax of 40 percent.

The question of whether or not an inheritance recipient will be required to pay taxes is a multifaceted one. If the assets that comprise the estate do not exceed $5.34 million in value, the estate as a whole will not be taxed. So the answer is no on this level, when the estate is worth less than $5.34 million.

If it was worth more, the individual beneficiaries do not pay the estate tax. The estate is responsible to pay the tax, so it comes out before other transfers, which means that the value of the estate as a whole would be reduced by the imposition of the tax.

Many laypeople would naturally think that an inheritance tax and an estate tax are exactly the same thing. They assume that these are just different terms that describe the same death tax.

In fact, an inheritance tax is something that is by definition different from an estate tax. As we have already touched upon, an estate tax is imposed on the entire estate. An inheritance tax is levied upon each person receiving an inheritance.

Fortunately, there is no inheritance tax in the United States on the federal level and as mentioned above, we do not have a state level inheritance tax in the state of Nevada. However, there are some states in the union that do have inheritance taxes. As we said, the beneficiaries of the estate typically pay an inheritance tax in those states. State level estate taxes are typically paid by the estate, similar to the federal estate tax.

In fact, residents of New Jersey and Maryland are faced with the prospect of paying a state level estate tax, a state level inheritance tax, and the federal estate tax.

It should be noted that states that have an inheritance tax generally exempt very close relatives like spouses and children.

You may wonder if you are going to be forced to report an inheritance on your annual tax return claiming it as income. If you receive a bequest, generally speaking it is not going to be looked upon as taxable income.

However, if the inheritance was to appreciate during the administration process before it was distributed, the gains could be taxable. Similarly, if income is generated during that time, it could be subject to income tax.

Of course, if you sell property that you inherited at a later date after it appreciated, the capital gains tax would be a factor, but the cost basis is stepped up to the value as of the date of the deceased owner's death, so the tax would only be for the appreciation after that date.

This post provided a little bit of information about estate planning and taxation in Reno Nevada. To learn all of the details, contact our firm to schedule a free tax efficiency consultation.

It can be intimidating to consider the possibility of relinquishing control over your property. People sometimes assume that you do surrender control of assets when you create a trust.

It can be intimidating to consider the possibility of relinquishing control over your property. People sometimes assume that you do surrender control of assets when you create a trust.

In this post we will provide some clarity about creating a trust in northern Nevada.

There are different types of trusts. Perhaps the most commonly utilized trust in Reno NV in the field of estate planning is the revocable living trust.

These trusts are largely useful to enable probate avoidance. If you use a last will to state your final wishes, the estate must be probated before your heirs receive their inheritances.

This process can be expensive and time-consuming. Most people would like to facilitate timely asset transfers.

When you use a revocable living trust to arrange for these transfers the distributions to the beneficiaries will take place outside of probate.

Because of the fact that the trust is revocable, you do retain control of assets that you convey into this type of trust.

You can act as both the trustee and the beneficiary while you are still living, and most people will do this. As a result, you can control investments and give yourself distributions as you see fit.

The control doesn't stop there. Because the trust is revocable, you can actually dissolve or revoke it at any time. The terms that you originally set forth are not etched in stone either. You can change them and add or subtract beneficiaries.

There are irrevocable trusts as well. With some exceptions, these trusts do require you to surrender incidents of ownership, so you do not continue to have control of the property that has been conveyed into the trust.

Because the trust is not revocable, you cannot dissolve it, and generally speaking the terms cannot be changed.

Why would you want to create a trust that did not allow you to retain control? There are a number of reasons.

Certain estate tax efficiency strategies involve irrevocable trusts. Because the assets would be owned by the trust rather than the estate, there are certain benefits.

In addition, when you surrender incidents of ownership by placing assets into an irrevocable trust they are generally going to be protected from creditors and claimants seeking redress. Nevada does allow some irrevocable trusts to be "self-settled," so some incidents of ownership are retained, but these are sophisticated strategies that require the advice of competent counsel to establish and fund.

The best way to proceed if you have questions about estate planning would be to discuss everything in detail with a licensed Reno Nevada estate planning lawyer.

Rather than looking for answers to general questions about what trusts can and cannot do, you would be better off consulting with an attorney. You can explain exactly what you want to accomplish, and your attorney can give you direct answers to your specific questions.

November 11 is Veterans Day, and people around the country are taking some time to remember the contributions that have been made by former service members. In this post we would like to share some thoughts about retirement and estate planning for veterans.

The Basics

Veterans have the same concerns that we all do when it comes to estate planning. You want to make sure that you are taking all the appropriate steps with regard to the transfer of your assets after you pass away. It is also important to be financially prepared for the different stages of life.

When it comes to the latter component, if you are a careerist you have some great opportunities when it comes to retirement planning. The military pension that service members are entitled to after at least 20 years of service can be a fantastic supplement to Social Security income.

In addition, many people embark on careers in the private sector after serving 20 years. If you joined up after college at the age of 22 for example, you would be just 42 when you leave the service.

You would have an extraordinary resume. Your undergraduate education would have been in place before you joined, and you may well have added onto that while you were in the military.

This presents an extraordinary opportunity for wealth building. You could be drawing a significant retirement pension while you are traversing a civilian career path. If you plan ahead effectively, you could potentially accumulate quite a bit of wealth while you enjoy a comfortable lifestyle.

This would all lead to the ability to enjoy your retirement years to the utmost once you decide to put your working years behind you.

Legacy Planning

Service members are inherently involved in history making. When you have served in the Armed Forces, especially during a time of war, you have experienced things that civilians simply cannot fully grasp.

A legacy plan can involve leaving behind autobiographical notes or memoirs. This can be a gift that has a lasting impact that transcends dollars and cents.

Veterans should definitely consider putting their experiences into writing. You can include these memoirs among your estate planning documents. Family members can learn much, and perhaps ancestors yet unborn can learn some history when they read your reminiscences.

There is also the matter of physical mementos. Veterans often retain ownership of items that hold a great deal of significance to them. When you share the stories that are attached to things that you will be leaving behind, you imbue these items with meaning that can be felt over the generations.

Honoring Veterans

We would like to thank all veterans for their service. Without their sacrifices we would not have the freedoms that we enjoy each and every day.

During 2010 the estate tax was temporarily repealed. This repeal was in place due to provisions that were included in the Bush era tax cuts.

Under the laws as they existed during 2010, the estate tax would return in 2011. The amount of the federal estate tax credit or exclusion would be just $1 million. The top rate for estates in excess of $1 million was scheduled to come in at 55 percent.

In 2009 the estate tax exclusion was $3.5 million, and the top rate was 45 percent. It seemed that come 2011, we would be facing a huge tax increase.

Fortunately, in December of 2010 a new tax relief measure was passed through Congress. This measure is called the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010.

Under terms contained within this act, the estate tax exclusion was set at $5 million for 2011 and 2012. Ongoing annual adjustments for inflation were mandated. A maximum rate of 40 percent was put into place. The law was scheduled to sunset at the end of 2012 again, but fortunately Congress made it permanent in 2013.

Incremental Increases

For 2012 the Internal Revenue Service raised the exact amount of the federal estate tax exclusion to $5.12 million to account for inflation. Another adjustment was applied in 2013, bringing the amount of the exclusion up to $5.25 million.

2013 is rapidly coming to a close, so the IRS has announced the amount of the estate tax exclusion for 2014. An additional $90,000 will be added to the existing $5.25 million exclusion. Next year the exclusion will be $5.34 million.

Exclusion Afforded to Each Taxpayer

It should be noted that this is a per person exclusion. Each individual taxpayer is entitled to an exclusion of $5.34 million. As a result, if you are married you and your spouse would have a combined exclusion amount of $10.68 million next year.

If you were to pass away next year, your spouse can take some legal steps that would still allow him or her to have a total exclusion of $10.68 million, because the estate tax exclusion is portable between spouses.

Annual Gift Tax Exclusion

In addition to the estate tax there is also a federal gift tax. The two taxes are unified. The $5.34 million exclusion that we will see next year will apply to transfers by gift during your life or by inheritance at death. Because it covers taxable gifts that you give while you're living along with the value of the assets that will be passed to your heirs after you die, the gifts you make that are in excess of the annual exemption will reduce the exemption amount at your death.

The annual gift tax exclusion is the amount you can give without filing a gift tax return or reducing your estate tax exclusion. You don't use up any of your unified lifetime exclusion unless you make a gift to a single person during a calendar year that exceeds the amount of this annual exclusion.

During 2013 the amount of this exclusion has been $14,000. Because of the fact that the Internal Revenue Service raised the lifetime unified exclusion, you may wonder if the annual gift tax exclusion was increased as well.

Unfortunately, the annual gift tax exclusion is not going to be raised for the 2014 calendar year. The $14,000 figure will remain in place next year. Remember, however, it is a per person exclusion, so you and your spouse can gift $14,000 each to your daughter and her husband, a total of $56,000 per year without filing a return or adversely affecting your lifetime exemption.

Probate stands in the way of your heirs and their inheritances when your assets are in your name at the time of your death. Nevada probate can take a significant amount of time (often a year or more), and most people would like their heirs to receive their inheritances in a more timely manner. For some, this wait is not a problem. For other families, however, there may be an immediate need for liquidity.

Probate stands in the way of your heirs and their inheritances when your assets are in your name at the time of your death. Nevada probate can take a significant amount of time (often a year or more), and most people would like their heirs to receive their inheritances in a more timely manner. For some, this wait is not a problem. For other families, however, there may be an immediate need for liquidity.

The waiting period is only one of the problems with the Nevada probate process. Expenses can accumulate during this process , and they can ultimately consume a noticeable percentage of the estate (often 4% - 8% or more if there is a contest). This is all money that could have gone to the heirs if probate was avoided.

It is possible to avoid probate in Nevada. There are a number of ways to go about it, and one of the most popular probate avoidance solutions is the revocable living trust.

Once you convey assets into the name you have given to your revocable living trust you name a trustee that is empowered to manage the assets that are titled in the trust. You also name a beneficiary or beneficiaries who would receive distributions out of the trust. The nature of these distributions would be decided by you when you create the trust agreement.

Initially you may serve as both the trustee and the beneficiary. By doing so, you do not surrender control or beneficial use of the assets. You can distribute assets to yourself, manage your own investments, and change the terms of the trust agreement if you want to do so. Since the trust is revocable, you can even revoke it entirely if you ever choose to do so. Since the point is to facilitate the transfer of your financial assets after you pass away you name a successor trustee, and you name beneficiaries who will receive distributions out of the trust after you die.

Once the assets have been conveyed into the revocable living trust they are no longer considered to be probate assets under the laws of the state of Nevada. As a result, when the trustee distributes monetary resources to the beneficiaries of the trust these asset transfers are not subject to the process of probate.

The creation of a revocable living trust is one way to avoid the probate process, but there are others as well. If you would like to discuss all of your options with a licensed professional please feel free to contact Anderson, Dorn & Rader, Ltd. to request a no obligation consultation.

We will listen carefully as you explain your objectives, gain an understanding of your unique personal situation, and make the appropriate recommendations. You can then go forward with a tailor-made estate plan that will facilitate a fast, efficient, and cost-effective transfer of assets to your loved ones when the time comes. To learn more, please download Anderson, Dorn & Rader, Ltd.'s free probate process report.

There are different types of wills that are used in the field of estate planning. One of them is the last will or last will and testament, which is used to transfer assets following your death. You can also nominate a guardian for dependents in your last will. Another type of will that should be a part of every comprehensive estate plan is a living will. Some people confuse living wills with living trusts, so we would like to provide some clarity here.

Individuals generally equate a will with the transfer of property. This can lead to the misconception that a living will facilitates property transfers while you are still alive.

This is not the case. A living trust is a vehicle of asset transfer. However, a living will has nothing to do with financial matters.

With a living will you state your wishes with regard to the implementation of life-sustaining measures like the utilization of feeding tubes, respirators, and ventilators.

It seems that modern medicine can keep people alive almost indefinitely using these measures, even if there is no hope of recovery. Some individuals would want this to continue, and others would prefer to allow nature to run its course. How you feel about it is a personal preference, and you can state that preference by executing a living will.

If you don't have a living will and you do fall into an incapacitated state your closest relatives would be forced to make decisions in your behalf. This is a very difficult position to be placed in. You essentially have a matter of life or death in your hands, and you may not know how the person in question would have acted if he or she could communicate.

Disagreements among family members often arise, because this is an issue about which people can be very passionate. This is a difficult time for all concerned, and family members should be pulling together. You can prevent this type of situation if you take the time to execute a living will.

A living will is an advance directive for health care. Since we are covering an important advance directive in this post we would like to mention another one that is highly recommended, the health care power of attorney.

Medical decisions may present themselves that are not specifically covered in the living will. They may be quite sensitive. You can appoint someone of your choosing to make these decisions for you if it becomes necessary by executing a durable power of attorney for health care.

When you do this the agent you name will have the legal authority to act on your behalf when it comes to health care decisions.

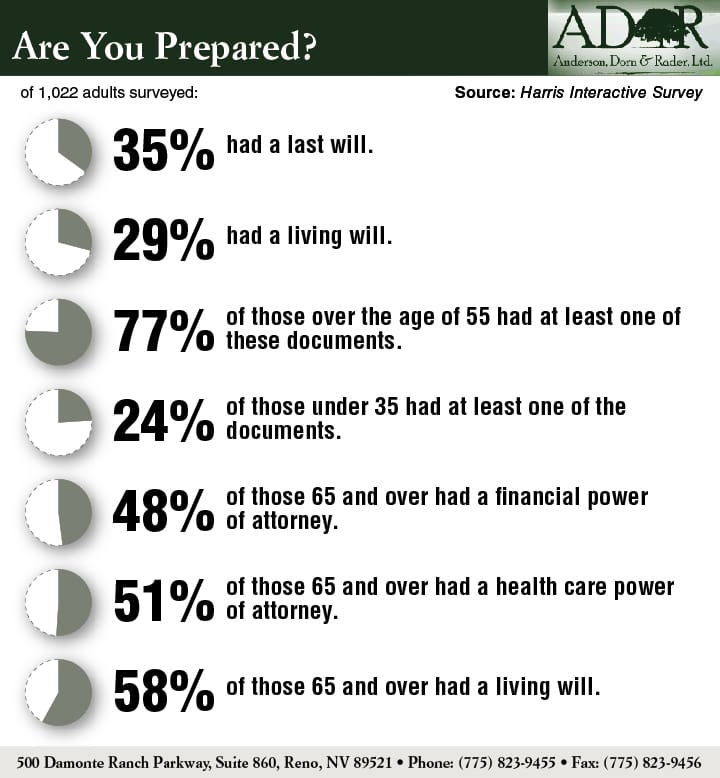

35% had a last will.

29% had a living will.

77% of those over the age of 55 had at least one of these documents.

24% of those under 35 had at least one of the documents.

48% of those 65 and over had a financial power of attorney.

51% of those 65 and over had a health care power of attorney.

58% of those 65 and over had a living will.

Click here to view a larger image.

Wealth preservation involves the deployment of estate tax strategies. To determine whether or not your wealth is potentially subject to the estate tax before it is passed on to your heirs you should be aware of the federal estate tax exclusion.

For the rest of this year the estate tax exclusion is $5.25 million. The maximum rate of the federal estate tax is 40% under the provisions of the American Taxpayer Relief Act of 2012. (Ironically, prior to this "relief" the maximum rate was 35%.)

Under existing laws the estate tax exclusion can be adjusted annually for inflation if such an adjustment is warranted. As a result you may see a slightly different estate tax exclusion amount in 2014 and in subsequent years assuming existing laws remain in place.

In addition to the federal estate tax we have a federal gift tax. It carries the same top rate, and it is unified with the estate tax. As a result, the $5.25 million exclusion is a unified exclusion. It applies to taxable gifts and your estate's value. For this reason giving gifts using this exclusion throughout your life is going to reduce the estate tax exemption at death, so you have to determine which is the best approach for you.

The good news is that there is an annual per person gift tax exclusion that exists separate from the lifetime unified exclusion. The exact amount of this exclusion does not necessarily remain constant every year, but in 2013 the amount of this annual per person exclusion is $14,000.

As a result, if you wanted to write a $14,000 check and give it to your son this transaction would not be taxable, and your lifetime unified exclusion would not be reduced by the value of the gift.

This is an exclusion that is afforded to each taxpayer. So, a married couple could give as much as $28,000 to any number of gift recipients this year free of taxation. If you had several children, friends or others to whom you wish to make gifts, you could transfer quite a bit of money tax-free, and you could also give tax-free gifts to their spouses using this annual exclusion.

The estate tax exclusion is portable. This means that the surviving spouse could use the unused portion of the exclusion that his or her deceased spouse was entitled to.

When you're planning your estate you should be aware of the fact that there is an unlimited marital deduction. You can give your spouse any amount of money while you are living free of the gift tax. Your spouse can also inherit any amount of money from you without incurring any estate tax exposure.

An estate consists of the assets you own at any given time. It is your estate that you will leave behind after you pass away. Estate planning is the process of providing for the appropriate distribution of the assets that will comprise your estate in the event of your death.

Many people will think about estate planning and immediately equate it to the execution of a last will. A last will is utilized to express your final wishes with regard to the distribution of your assets.

When you draw up a will you must also choose a personal representative (historically, called an executor or executrix). This is the individual that will administer the estate.

You should choose your personal representative wisely because it is not just a ceremonial role. The personal representative must guide the estate through the process of probate. During probate final debts must be settled, and property must be inventoried and in some cases liquidated before it is divided and distributed among the heirs of the estate.

Because of the business that must be conducted the personal representative should be someone who is comfortable taking care of these tasks. There could be a good bit of time involved so you should also select someone who has the time to do the job.

A last will is not your only option for transferring assets at your death. Because wills must be probated through the courts and probate is time-consuming many people choose to avoid it by arranging for asset transfers using methods other than a last will.

A popular choice for probate avoidance is a revocable living trust. With these trusts you retain control of the assets while you are alive by acting as both the trustee and the beneficiary.

After you pass away, a successor trustee distributes assets to the beneficiaries that you choose according to your wishes. These asset distributions take place outside of the probate court.

There are other types of trusts that can be used beyond revocable living trusts. The correct choices vary on a case-by-case basis depending on the objective of the person creating the estate plan.

People who are in possession of considerable wealth have to concern themselves with the federal estate tax. This tax carries a 40% rate , and in 2013, the amount of the exclusion is $5.25 million.

It is possible to position your assets in a way that mitigates your estate tax exposure if you work with a licensed estate planning attorney.

In addition to the estate tax concerns, other estate planning objectives include asset protection, special needs planning, and spendthrift protections.

Every responsible adult should have an estate plan in place. This is something that you are doing for the benefit of your loved ones, and you could be leaving a potentially difficult situation behind if you don't take the appropriate steps in advance.

The Sopranos television series obviously generated a lot of revenue, and as you might imagine "Tony Soprano" James Gandolfini left behind a considerable estate. At the time of his passing his net worth was estimated to be approximately $70 million.

The accumulation of wealth can result in a great deal of estate tax liability if you don't take the correct steps to position your assets with wealth preservation in mind.

Apparently the actor did not plan ahead very effectively. He did have an estate plan in place, but most of his wealth is being transferred under the terms of a last will. Simply creating a simple will to direct the transfer of assets is not going to do anything to provide you with estate tax efficiency.

On the federal level the estate tax carries a 40% maximum rate, and the current exclusion is $5.25 million. Gandolfini resided in New York, so his family faces yet another layer of taxation because there is a state-level inheritance tax in the state of New York.

The New York state inheritance tax exclusion is $1 million, and the maximum rate of the tax is 16%.

When you combine the rates on both the federal and the state level you are looking at total taxation that consumes more than half of the taxable portion of an individual's estate.

In the case of James Gandolfini it is estimated that his heirs will receive only $40 million out of the $70 million that he left behind after estate taxes have been paid. With proper planning, there is a good possibility that the entire estate tax liability could have been avoided. Unfortunately, most of us rationalize our procrastination until we have a "wake up call" such as a personal medical event or the death of a loved one. Gandolfini was not elderly and had little forewarning, so he likely thought he had time to consider his estate planning. Perhaps, his untimely death and the tremendous costs associated with it will be the wake-up call more of us need to meet with qualified counsel and complete our estate planning before the unfortunate event occurs.

When you see some of the estate planning failures that have been taken by others, you may be motivated to avoid the same mistakes. People sometimes fail to plan ahead for the inevitable because they are under the impression that they are too young to concern themselves with estate planning. While it is obviously true that people in their 30s do not usually pass away, sometimes they do. It is not entirely uncommon for younger people to pass away in motor vehicle accidents. Catastrophic illnesses sometimes strike, and there are those who are the victims of criminal acts.

When you see some of the estate planning failures that have been taken by others, you may be motivated to avoid the same mistakes. People sometimes fail to plan ahead for the inevitable because they are under the impression that they are too young to concern themselves with estate planning. While it is obviously true that people in their 30s do not usually pass away, sometimes they do. It is not entirely uncommon for younger people to pass away in motor vehicle accidents. Catastrophic illnesses sometimes strike, and there are those who are the victims of criminal acts.

Longtime NFL quarterback Steve McNair was unfortunately in the latter category. He was killed in 2009 by his mistress when he was just 36, and he left behind a wife and children. He did not have a last will expressing his final wishes. All responsible adults should have an estate plan, but it becomes absolutely essential when you are a married person with children depending on you. You may feel that things automatically fall neatly into place, but this is simply not the case. While Steve McNair did in fact have significant financial resources, his assets were frozen by the probate court because he did not have a will, a trust, or any other estate planning documents in place. His assets were frozen in large part because of his estate tax exposure. He could have taken steps to mitigate this exposure while he was still alive through proper estate planning. The federal estate tax carries a 40% maximum rate so it can certainly play havoc with your financial legacy. Another individual who was victimized by this lack of planning was Steve McNair's mother, Lucille.

McNair was apparently quite grateful to his mother for all the things that she had done for him while he was growing up. During the prime of his career he was a superstar with the Tennessee Titans, and he was in a position to provide his mother with the home of her dreams. He built her a ranch in Mississippi that sat on 45 acres. Lucille looked upon this home as a gift that was given to her by her son. However, the fact is that Steve McNair kept the home in his name. His mother was not the legal owner of the home at the time of his passing. As a result, the home was looked upon as probate property. Steve McNair's widow was named as the personal representative or executor of the estate by the probate court. She demanded $3000 a month rent for the property, and Lucille could not pay so she had to move. It is unlikely that Steve McNair would have wanted to see this outcome. He could have prevented it if he would have taken the time to construct his estate with the assistance of a licensed estate planning attorney.

Don't be another estate planning failure and speak with an experienced Estate Planning Attorney at Anderson, Dorn & Rader, Ltd. Contact us online or call (775) 823-9455 to set up an appointment.

You should be aware of the process of probate in Nevada when you are making preparations for the distribution of assets to your loved ones after your passing. When you hear some of the details you may decide that you would like to take steps to avoid probate.

If you have a will, it is filed by the executor and is reviewed by the court to determine its validity. If there is no will, the probate court will follow the "will" found in the statutes of the state where you reside. These are call the laws of intestate succession. During the probate process final debts of the deceased must be reviewed, allowed or challenged and, after approval by the court, paid by the executor out of estate funds.

This can include the payment of taxes, so services of an accountant are often necessary. Certain assets may need appraisals, and this can require the engagement of an appraiser or appraisers.

Because probate is a legal process the executor is also going to need the assistance of a probate lawyer in many cases.

When you add up the fees that will be charged by all these professionals they can be considerable. Further, the executor who is administering the estate is entitled to payment for his or her time and trouble.

One reason to avoid probate is to avoid these costs. Another is to reduce the time spent in administration that increases the wait for distribution to the beneficiaries.

Some people decide they want to avoid probate and they do it by adding a co-owner to property and financial accounts. This is called joint tenancy with right of survivorship.

The idea is that the surviving joint tenant inherits the property in question after the death of the other co-owner, without the need for probate.

There are a number of risks you take if you were to go this route.

Let's say that you make your brother the co-owner of your property. Someone sues your brother. The property you have worked for all of your life is suddenly fair game for the litigant seeking redress.

Another risk you take is that the person you add to your bank account has total access to the funds. Clearly you are going to select someone that you trust, but their creditors also have total access.

These are a couple of things to think about, but there are many other unintended consequences that can result if you use joint tenancy as an estate planning solution.

The creation of a revocable living trust would be a better way to avoid probate. You as the creator of the trust are called the "trustor" or "settlor." While you're living you can act as the trustee and the beneficiary so you have sole control of the assets.

Because the trust is revocable you can dissolve it if you wish, or amend and change the terms at any time. After your passing the trustee you choose to succeed you when you create the trust becomes the trustee. He or she then administers the estate outside of the courtroom and distributes the assets to the beneficiary or beneficiaries in accordance with your expressed wishes.

The process of estate planning involves some very measured and informed decision-making. If you make certain assumptions as a layperson you may be making errors of commission and omission.

Because of the fact that there are websites on the Internet selling do-it-yourself generic, fill-in-the-blanks last wills, more and more people are getting the idea that they can go it alone. Unfortunately, this is increasing the numbers of people who are not properly prepared.

With a will, you need to consider the fact that your estate must be probated before the heirs receive their inheritances. The probate laws in the state of Nevada require rigid formalities that may cause delay and expense if they are not followed precisely.

When you work with a qualified estate planning attorney who is licensed in Nevada you can be certain that your will is properly constructed.

If you use a boilerplate document that you picked up on the Internet or at the book store you have no way of knowing if the will is truly up to par.

And then there is the simple fact that a last will may not be your best choice.

Last Will Alternatives

The probate process that we mentioned above is time-consuming, and, when all the costs, fees and expenses are considered, quite expensive.

There are effective ways to arrange for asset transfers to your heirs directly, outside of probate. One of them would be through the creation of a revocable living trust.

With these trusts you can retain control of the assets while you are alive and well. If you were to become incapacitated, your successor trustee would be empowered to handle your financial affairs, usually avoiding the need for a guardianship.

Upon your passing the trustee administers the estate outside the probate court and then distributes assets to the beneficiaries in accordance with your wishes.

Specialized Concerns

There is no one-size-fits-all estate plan because different families have different concerns. For instance, if you have estate tax exposure you must take steps to position your assets in a tax efficient manner to avoid a 40% hit.

If asset protection is a concern you would implement certain strategies that would not be important if you were not concerned about shielding assets from creditors and litigants.

Special needs planning is a factor for some people. You have to be careful about the way you set aside money for a person with a disability who is relying on government benefits like Medicaid and Supplemental Security Income.

People who are owners of small businesses are going to have estate planning concerns that differ from those who work for someone other than themselves.

These are just a few examples of the unique circumstances that require varied approaches.

Decision Makers

It is also important to include an incapacity component within your estate plan. The courts could, at considerable expense to your estate, appoint a guardian to manage your affairs if you don't take the appropriate action. This guardian may not be someone that you would have chosen.

You can select potential future decision-makers using an appropriate revocable living trust combined with a durable power of attorney.

All these solutions are best handled with a qualified estate planning law firm.

There are numerous federal government benefits that legally married same-sex couples have traditionally been unable to enjoy. Even though a number of states sanction same-sex marriages, the federal government has not recognized them.

This is because of provisions contained within the Defense of Marriage Act (DOMA).

One of the benefits that has not been extended to same-sex spouses is the unlimited marital estate tax deduction. If you are legally married in the eyes of the federal government you can transfer any amount of money to your spouse without incurring any estate tax liability.

Back in 2009 a New York woman named Thea Spyer passed away and left her spouse, Edith Windsor, a significant sum of money. The two women had married in 2007 in Canada after being together for decades.

The Internal Revenue Service imposed the estate tax.

Edith Windsor took legal action, challenging the constitutionality of the portion of DOMA that strictly defines marriage as a union between a man and a woman. She cited the equal protection clause in the Constitution.

The Supreme Court sided with Edith Windsor's contention by a 5 to 4 vote.

As a result the matter of whether or not gay marriages are legal will be left up to each individual state to decide. The federal government will indeed start to recognize these marriages, and benefits like the unlimited marital deduction will be available to legally married same-sex spouses.

If you have questions about how this ruling may impact your existing estate plan contact our firm to schedule a free consultation.